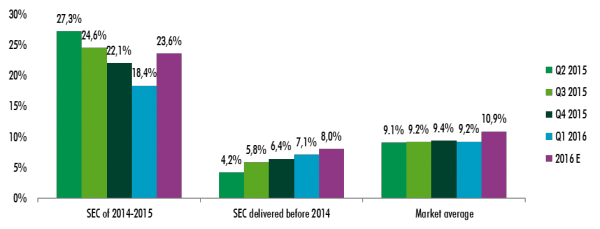

Average vacancy rates across shopping centre stock in Moscow dropped by 0.2ppts in Q1 2016, driven by new centres revealing the biggest drop to 18.4% from 21.2%.

According to CBRE’s Moscow Retail Market report average vacancy rate across the market dropped to 9.2% by the end of Q1, however centres delivered earlier than 2014 saw an increase to 7.1% from 6.4%.

Vacancy rate in different shopping centres, %

Source: CBRE

In Q1 2016 no new shopping centres have been delivered in Moscow. Until the end of 2016 at least six shopping centers with high stage of readiness are expected to be opened: Okeania (ex- Gallery Kutuzovskiy, 60,000m2), Khorosho (52,000m2), Butovo Mall (57,000m2), Riga Mall (80,000m2) and the 2nd phase of Fashion House Outlet (4,500m2). Riviera (100,000m2 rentable area) opened in Moscow on 15 April 2016.

Taking into the account the number of new shopping centres to be delivered in Moscow Region in 2016 by the end of 2016 the average vacancy rate in Moscow shopping malls may increase to 11%, as the new projects is expected to open with 40-60% vacancy rate. Prime rental rate in Moscow shopping centres in Q1 2016 remains at $1,650/m2/year.

Q1 2016 key Moscow Retail market indicators

|

2015 |

Q1 2016 |

2016 F |

|

|

Total stock, ‘000 m2 |

5,244 |

5,244 |

5,594 |

|

Completions, ‘000 m2 |

441 |

0 |

350 |

|

Vacancy rate in SCs, % |

9.5 |

9.2 |

11.0 |

|

Prime capitalization rate, % |

10.25 |

10.25 |

10.25 |

Source: CBRE

In Q1 2016 the retailer activity remained at the level of H2 2015. Eight new international brands opened their first store in Moscow in Q1 2016. In addition, six new international retailers announced their plans to enter the market during 2016: Walt Disney, Newby London, Lillapois, NYX, Hunkemöller and Undiz. Among foreign brands, Stockmann announced in Q1 their plans to close their Lindex stores.

Olesya Dzuba, director, strategic analysis and planning department CBRE in Russia, commented: “New shopping centres are now offering very favorable commercial terms for new outlets opening. That was the reason for the vacancy rate decline in new shopping centres, which usually are represented by modern design and concept, better thought out floor plans, enough parking slots. The main factors forming the rental payment in the shopping center under construction are its stage of construction and occupancy rate, the concept quality and its positioning, which are directly effecting the retailer turnover.”