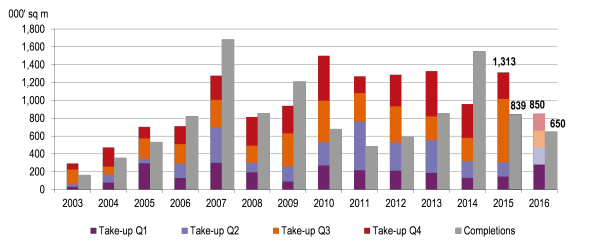

Only three high quality warehouses with the total area of 92,000m2 were commissioned over the first three months of 2016 in the Moscow region, almost four times less compared to completions over the same period last year according to JLL.

Among the largest deliveries in Q1 there were new premises in PNK – Severnoye Sheremetyevo (54,000m2 of warehouse space) industrial park and Synkovo logistic park (28,000m2). The biggest upcoming projects in 2016 are new premises in South Gate industrial park (100,000m2) and Radumlya logistic park (70,000m2).

In the longer term, further decline in the amount of new deliveries is expected. For the full year, the total volume of new supply of warehouse space in Moscow is expected to be close to 650,000m2 which will be 23% lower than in 2015. The bulk of future supply in 2017-2018 is represented by built-to-suit schemes, indicating construction begins only in the case of actual demand for warehouse space.

Demand and Supply of Warehouse Market in Moscow Region

Source: JLL

Several large transactions originally expected to be completed in late 2015 and postponed to Q1 2016 contributed positively to the total take-up volume in Q1, which were 280,000m2 compared to 146,000m2 in Q1 2015. The average size of a warehouse deal was 14,000m2, which was slightly less than the average size in 2015 (16,400m2). The main drivers of demand for new warehouse space in Q1 were retailers and logistics companies, accounting for 46% and 34% of all transactions respectively.

In terms of geographical location, the demand for warehouse space was predominantly in the southern and northern directions, where active recent construction in recent years resulted in large volumes of new supply of warehouse space.

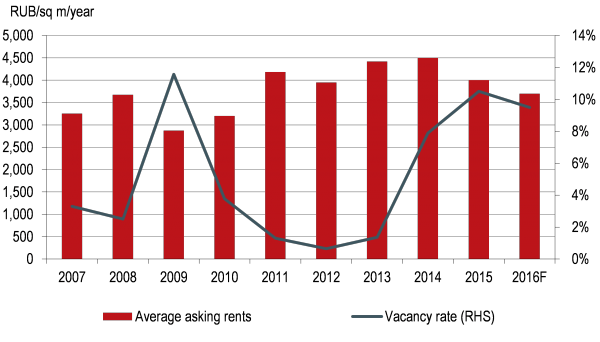

Despite considerable demand in Q1 2016 coupled with the decreasing supply, the vacancy rate in existing warehouse premises saw almost no change both in QoQ and YoY terms and stood at 10.2% versus 10.5% at the end of 2015 and 10.4% in Q1 2015.

"The occupier activity was seen mainly on the secondary market, as tenants were moving out of expensive stock to more affordable new warehouse premises. This process, however, did not affect net absorption and led to a significant increase in vacant space on the secondary market” commented Petr Zaritskiy, regional director, head of warehouse and industrial department, JLL, Russia & CIS.

“At the same time, due to demand for warehouse space, particularly from food retailers, the amount of take-up this year is unlikely to fall below 850,000-900,000m2, which will likely lead to a gradual decline in the overall vacancy rate to 9-9.5% by the end of 2016."

Warehouse Market Balance in Moscow Region

Source: JLL

Over the course of Q1, the average level of asking rents for new deals in Class A decreased by 7.5% QoQ to RUB3,700/m2/year (triple net). The level of prime rents stood unchanged QoQ at RUB4,200/m2/year (triple net). The actual level of rents varies quite significantly depending on particular object and its location, with relatively expensive supply located on the most demanded locations (eg close to Moscow Small Ring highway).