Dublin’s flexible office sector is experiencing a significant boost, with increasing demand driven by evolving workplace strategies and a focus on collaboration and company culture, according to a new report from CBRE Ireland.

The flexible office market in Dublin continues to see robust growth, with occupiers shifting towards more fluid working models in the post-pandemic landscape, according to commercial real estate specialists CBRE Ireland. Their latest report reveals key insights from a survey of the city’s leading flex office operators, highlighting strong demand, high occupancy rates, and a steady pipeline of new openings.

Market Overview

The report notes that the Dublin flex office sector recorded nearly 7,300 m² (€600-€800 per desk per month) in take-up during 2024, with notable deals including Iconic Offices’ new space at 3-8 Hume Street and xDanu's long-term lease at The Freight Building with landlord Glenveagh Properties.

Survey Findings

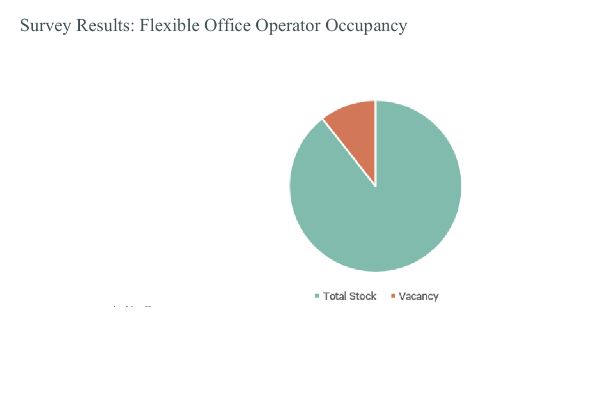

As part of their research, CBRE Ireland hosted a session in Q1 2025, surveying 13 leading flexible office operators who collectively manage 117,690 m² (1.3m sq ft) of office space, equating to more than 21,000 desks across Dublin.

Key findings from the survey include:

-

Over 60% of respondents cited ‘Financial & Professional Services’ as the main driver of demand in 2024.

-

Average occupancy rates were strong at nearly 80%, excluding early-stage startups.

-

54% of clients required 15-25 desks, while another 15% sought 25-50 desk spaces.

-

Operators recorded an average of 324 desk sales annually.

Prime Locations & Expansion Plans

Premium flex office providers continue to thrive, with Grafter at 6-7 St. Stephen’s Green and IPUT Real Estate's Making it Work concept maintaining high occupancy. Meanwhile, 2025 will see Whitefire launching a new space at 19-21 Aston Quay in Dublin 2.

Alternative Deal Structures Gaining Traction

According to Dan Shannon, Executive Director at CBRE Ireland’s Office Tenant Advisory team, “There has been an ongoing trend with new operators exploring the market but seeking to unlock transactions on alternative deal structures, including revenue shares and management agreements. In Dublin, total serviced office stock still accounts for less than 3% of the overall office market—considerably lower than other European cities. Whilst we have visibility on some granular growth over the next 12 months, supply is unlikely to increase significantly. We have seen continuous interest from new operators seeking to enter the market.”

Megan O’Donnell, Broker on CBRE Ireland’s Flexible Offices team, added: “Dublin-based flexible operators are seeing strong take-up and demand and low vacancy levels. Given the increased flexibility being offered by employers whilst also prioritising wellbeing and collaboration, we anticipate this trend will continue.”

Outlook

With demand for flexible workspaces remaining high and operators adapting to new leasing models, the Dublin flex office market is set for sustained growth in 2025. The sector's evolution presents new opportunities for landlords and operators looking to capitalise on changing workplace preferences.

Get the latest real estate news and investment insights from Europe Real Estate—your trusted source since 1999.

FREE subscription to receive daily or weekly updates. Sign up here!