The number of residential units transacted has almost doubled to 119,500 compared to the same period of the previous year, as recent months have been characterized by a number of large transactions. The four largest portfolio disposals of the first half year account for around three quarters of both the total transaction volume and number of units transacted. It is the first time since 2007 that we see such large transactions, e.g. the disposal of some 25,000 units from DKB Immobilien to TAG or the disposal of the 23,000-unit-plus Baubecon portfolio to Deutsche Wohnen AG. The fact that such transactions (can) currently occur in these numbers is explained by the favorable conditions. Large residential portfolios are being offered for sale, investor demand is high and financing for such large transactions is also possible. In recent years, these criteria have not always been fulfilled-at least not simultaneously.

Yet, while transactions of packages including more than 1,000 units have increased, the number of smaller portfolios transacted has significantly declined. A total of 60 residential portfolios changed ownership in the first half of 2012 compared with more than 90 packages transacted in the same period last year. However, rather than a consequence of insufficient demand, this is primarily attributable to a lack of supply. Particularly in the core segment, the strong buying interest of recent years means that there is scarcely any product remaining on the market. Consequently, price levels have also markedly increased. It has not been uncommon to see multiples of more than 15 times the annual net rent paid for portfolios in the prospering conurbations.

Domestic investors are still the most active buyers

Just as in previous years, purchasers this year are predominantly based in Germany. Domestic purchasers accounted for more than 70% of the total transaction volume in the first six months of 2012. However, this is not due to foreign investors having no interest in German residential property. On the contrary, the German residential market is exceptionally attractive from the perspective of international investors and interest in residential portfolios in Germany is correspondingly high.

There are two principal reasons that explain this low proportion of foreign purchasers. Firstly, such purchasers are primarily interested in opportunistic investments or at least portfolios with upside potential. However, such investment opportunities are still relatively rare owing, among other reasons, to the high price expectations of current owners. Secondly, German purchasers often have access to more favorable financing structures either because they bring more equity capital or they can obtain debt capital at good conditions. Ideally, they can even do both.

As a result, they are able to submit higher offers during competitive bidding than foreign investors and the latter, despite their interest, do not always come to the fore. However, this might change soon when more opportunistic portfolios come onto the market due to restructuring of finance, particularly in the CMBS market.

Listed property companies and insurance companies the largest purchasers

Listed property companies and REITs were the largest purchaser group with a 43% share of the transaction volume and net investments of more than €1.5 billion respectively. Pension funds also invested a net amount of some €1.5 billion to claim second place in the rankings. Other purchaser groups with significant positive net investments were private equity funds (€640 million) and open-ended funds (€250 million). The largest net vendors by far were banks, to which some portfolios had reverted from insolvent owners. Their net balance from portfolio disposals stood at almost €3.9 billion.

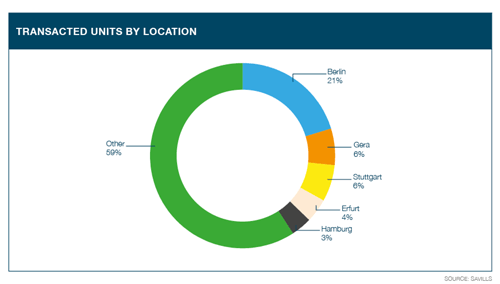

Berlin is the investors’ favorite

Berlin is without doubt the favorite location among investors at the moment. More than 24,000 residential units were transacted in portfolios in the capital in the first half of the year. This represents 20% of all units transacted in Germany. Berlin is followed by Stuttgart (6%) and the Thuringian cities of Gera (6%) and Erfurt (5%). Stuttgart accounts for a large proportion of the LBBW portfolio while the other two cities were heavily represented in the DKB portfolio. Hamburg ranks fifth with just less than 4,200 units transacted.

The fact that only three of the major German cities–Berlin, Stuttgart and Hamburg–recorded noteworthy shares of the overall market is also explained by the scarcity of product in these markets. On the one hand, there is relatively little willingness to sell and, on the other hand, there is scarcely any new supply on the market. The latter is primarily reflected in the low number of developments transacted. Only four project disposals have been recorded in the current year, and this comes as a result of the immense purchasing interest, in particular in the core segment.

Increased development activity and a shift to B-locations expected

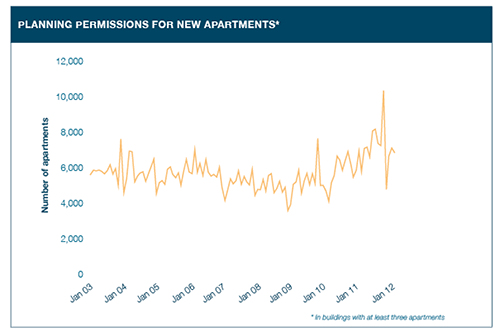

A glance at the planning permission statistics shows that this supply shortage may be relieved in the medium term. The number of units approved per month in the apartment segment has shown a clearly upward trend since the turn of the year 2009/10. Whereas some 4,000 to 6,000 units per month were approved across Germany in the years 2003 to 2009, this figure changed to 8,000 units during the course of 2011 and, at its peak, exceeded the 10,000 mark. This trend also indicates that the price rises in recent months have increased the profitability of residential projects and stimulated developers to take more projects forward.

The price levels now reached leave scarcely any upward room for maneuver. However, with demand likely to remain high and supply short, stability in prices is the most likely scenario. Owing to high prices in the large metropolises, it is also expected that investors will increasingly shift their attention to B-locations. Price increases in the major conurbations mean that these locations now offer more attractive risk-return ratios in some instances. Corresponding capital flows into the residential markets in these locations will surely be seen in the near future.

Is there a bubble?

Looking at the immense price increases in some cities, a few market observers are prompted to raise the question if there is a bubble in the residential market in Germany. For now, the answer to this question is: no! Some regions are hot for sure but generally, price increases are backed by corresponding increases in rents. Particularly the main conurbations, where investors’ demand is highest, saw a significant increase in rental levels over the past two to three years. However, investors should not assume that this trend will continue in the future. Rent increases in the past were based on strong economic fundamentals, i.e. a declining unemployment rate and rising wages. Against the backdrop of the economic slowdown further rent increases should be limited.

However, the German residential market remains attractive and 2012 will see the highest residential portfolio transaction volume since 2007. A double-digit total is still quite realistic, even if the transaction volume in the second half of the year turns out to be lower than that of the first six months. Much depends on whether any additional major transactions (e.g. the disposal of GBW, Woba or TLG) will be completed this year as overall supply remains scarce in the short term.

By Matthias Pink, Senior Consultant Research - Corporate Finance - Valuation, Savills Germany

About Savills

Savills is a leading global real estate service provider listed on the London Stock Exchange. Established in 1855, the company has today over 500 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East with 23,500 employees worldwide. In Germany Savills has six offices in Berlin, Düsseldorf, Frankfurt, Hamburg, Cologne and Munich. Savills provides expertise and market transparency to its clients in the following areas of activity:

• Purchase and sale of single assets and portfolios,

• Corporate Finance –Valuation,

• Leasing of office and retail buildings,

• Leasing and sale of industrial and warehouse properties

• Corporate Real Estate Services.