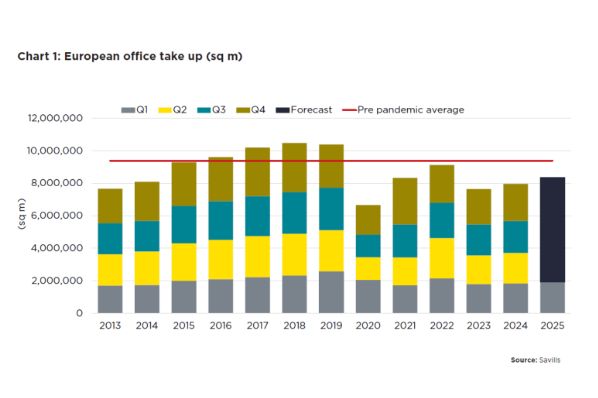

Office leasing across Europe is showing early signs of recovery, with Savills reporting a 4% year-on-year increase in take-up during Q1 2025, reaching 1.9m m². While this signals renewed demand in key urban markets, the sector faces a looming shortfall in new supply, with development completions expected to plunge to their lowest levels since 2017.

Performance was especially strong in Prague (+41%), Dublin (+29%) and London City (+26%), relative to their five-year averages. Germany’s top six cities posted a 13% rise in take-up, with Madrid recording its fourth consecutive quarter of stable activity. These markets are becoming increasingly competitive, particularly for energy-efficient, high-spec office assets.

“Average European office vacancy rates edged up by 10 bps during Q1 2025, reaching 8.4%, although this appears to be stabilising after several years of gradual increases. Vacancy is rising primarily in peripheral locations, while CBD locations remain considerably more resilient,” said Mike Barnes, Director at Savills’ European commercial research team.

A major concern for occupiers and investors is the dramatic fall in speculative pipeline. While office completions are projected to rise to 4.3m m² in 2025, they will sharply decline to just 3.1m m² in 2026. This scarcity of best-in-class stock is already pushing prime rents higher. Over the past year, London West End, Cologne and Paris CBD saw rent increases of 21%, 21% and 18%, respectively.

“The proportion of speculative deliveries as a percentage of total stock has dropped by half over the last three years to only 1.6%,” added Barnes. “New schemes are becoming let before completion, reducing the options available to occupiers and adding upward pressure on prime rents.”

While core cities offer more stable returns, many landlords in secondary markets are accelerating refurbishment strategies to meet tightening ESG standards and appeal to future-fit occupiers. “Investors continue to seek exposure to higher EPC rated office stock across European cities to maximise operational performance and adhere to fund requirements,” said James Burke, Director, Global Cross Border Investment at Savills. Central and Eastern Europe remains a hotspot, led by Bucharest (39%), Warsaw (37%), Budapest (32%) and Prague (27%) in new office stock built over the last decade.

People Mentioned:

-

Mike Barnes: Director, European commercial research, Savills

-

James Burke: Director, Global Cross Border Investment, Savills

Companies Mentioned:

-

Savills: International real estate advisor

Get the latest real estate news and investment insights from Europe Real Estate - your trusted source since 1999. To receive daily or weekly updates. Sign up here!