The Great Wall of Money | C&W

Available capital has now reached a new high of US$443 bn – with no limits to where this capital is flowing. Indeed, as all regions are targeted by this great wall of money, investment levels will likely reach record or near record levels in an increasing number of markets.

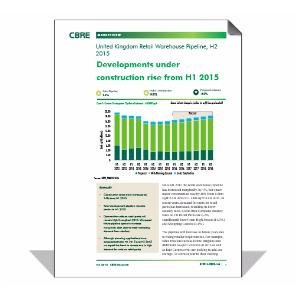

United Kingdom Retail Warehouse Pipeline, H2 2015 | CBRE

Since H1 2015 the retail warehouse pipeline has increased marginally, by 1%, but space under construction rose by 20% from .98m sq ft in H1 2015 to 1.18m sq ft in H2 2015. In recent years, demand for units on retail parks has increased, resulting in lower vacancy rates. Local Data Company vacancy rates on UK Retail Parks are 6.2%, significatnyl lower than High Streets (11.5%) and Shopping Centres ...

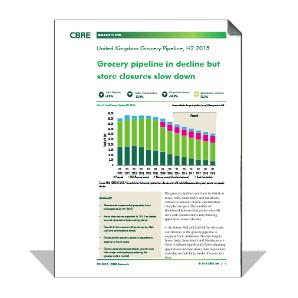

United Kingdom Grocery Pipeline, H2 2015 | CBRE

The grocery pipeline continues to shrink as Tesco, Asda, Sainsbury's and Morrisons reduce the amount of new supermarkets they plan to open. The number of abandoned schemes has grown since H1 2015 with constructions and planning application also in decline.

Investment Intensity Index | JLL

JLL’s Investment Intensity Index compares the volume of direct real estate investment in a city over a three-year period relative to the city’s current economic size. The Index provides a measure of real estate market liquidity, as well as a useful barometer of a city’s overall ‘health’, highlighting cities that are punching above their weight in terms of attracting ...

Capital Views - High Street Renaissance in Europe

Europe’s most luxurious high streets recorded another year of robust rental growth in 2015, according to research out from Cushman & Wakefield.

UK Big Box Industrial Report 2016 | JLL

This report provides a comprehensive round-up of market demand and supply, based on JLL's tracking of grade-A quality distribution units of 100,000ft² and over. Please note the take-up figures include build-to-suit (BTS) units only where planning permission has been secured. The report also comments on investment activity and yields.

Ireland Outlook 2016 | CBRE

2015 proved to be an exceptionally busy year in the Irish commercial property market following what was a record performance in 2014. Transaction volumes in the occupational and investment sectors of the market were impressive with annual average volumes of activity exceeded well before year-end in most sectors. Activity continued at pace throughout the year with several signifi cant portfolios ...

Globalisation and Competition: The New World of Cities 2015 | JLL

We are in a new era of city competition. The rigid global urban hierarchy is breaking down as cities increasingly specialise in niche markets, enabling more cities than ever to ‘go global’. This is fundamentally changing the geography of commercial property and has deep implications for real estate formats, assets and opportunities.

This paper, produced jointly by JLL and The ...