Investment: retail is the second least affected sector after hotels with €26.2bn invested in 2023

Investment in European retail fell 40% in 2023 vs 2022, to € 26.2b. Yet investor interest in retail assets is slowly gaining more traction in terms of investment market share (20% in Q4 23 vs 16% in Q4 22).

“This level has not been seen for five years (20% in 2018). As a result, retail was the second least affected sector after hotels”, said Patrick Delcol, Head of European Retail at BNP Paribas Real Estate.

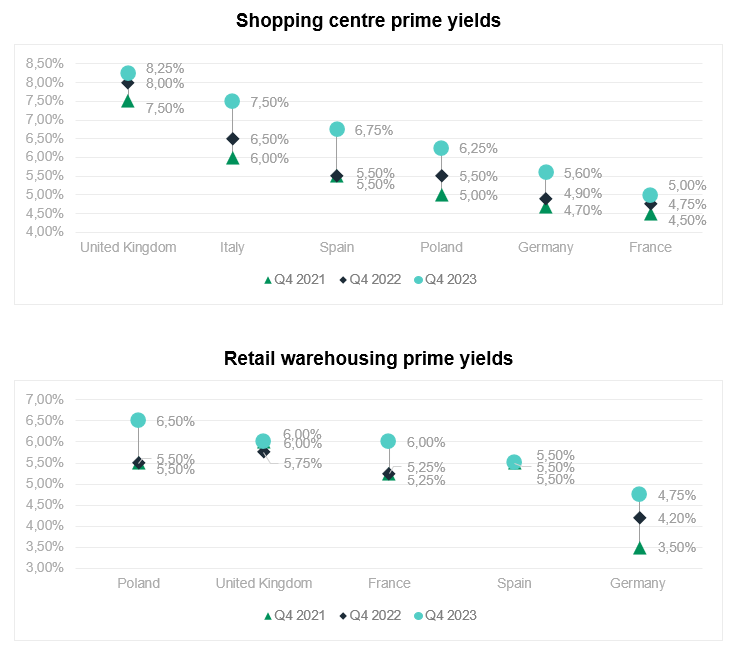

Attractive risk premium for retail warehousing and shopping centres

The rapid rise in risk-free rates in 2022 and 2023 has driven up prime yields, leading to repricing across all asset categories.

Retail prime yields started to expand in the second half of 2022 and continued throughout 2023. This yield expansion remains less pronounced than for other asset categories (office or logistics), as they had already adjusted at the time of the health crisis in 2020.

“Prime yields for retail warehousing and shopping centres remain very appealing throughout Europe and continue to attract investor interest. They are the segments that offer the best risk premiums of all real estate asset categories”, remarked Patrick Delcol.

High street prime yields remain the lowest despite having widened in most countries. This situation mainly reflects buoyant transactions in the luxury sector, which has weathered the crisis well. However, this niche market is far from reflecting the high-street segment as a whole, notably the struggling mass-market players.

With interest rates having peaked in late 2023 and central banks poised to lower them this year, investors should enjoy more favourable financing conditions, which should boost investment volumes in the second half of 2024, mainly by value-added and opportunistic players in need of leverage.

Luxury brands are still in the spotlight

In the occupier market, luxury brands are willing to pay a high price to access ultra-prime locations, as evidenced by the record rent signed by Yves Saint-Laurent on Bond Street in London. Store openings on European prime throughfares proliferated in 2023, such as Dior on Avenida de la Liberdade in Lisbon and Schiaparelli in the prestigious Harrods in London.

The reduced availability of prime locations drove up rents on luxury shopping streets in city centres. Rental growth is particularly noticeable in Milan (€13,000/m2/year, +16% in Q4 2023 vs. Q4 2022 on Via Montenapoleone) and in Rome (€11,000/m2/year, +15% on the Via dei Condotti). Rental growth also occurred in Vienna (€5,103/m2/year, +5% on Kohlmarkt) and Lisbon (€1,170/m2/year, +3% on Avenida da Liberdade). In Paris, prime rents are stabilising, although vacancy continues to decline.

Report provided by BNP Paribas Real Estate.

Image source - Pexels.

Written by: Ilona Klevansky Taillade