The UK is now set for an ‘In – Out’ vote on whether to remain a member of the European Union (EU) on 23 June 2016. Voting to leave (‘Brexit’) would represent a huge change in the UK’s political and economic relationship with the rest of the world.

Despite all the noise, the most likely result is that the UK will stay in the EU. Few of the polls so far have shown a majority in favour of leaving. In addition, telephone polls are generally showing a much stronger vote to stay in the EU than on-line polls (where the sample is more self-selecting and therefore those who feel strongly about the subject are much more likely to take part). The bookmakers’ odds also show a strong expectation that the UK will vote to stay in, with a ‘leave’ vote currently attracting 2:1 against (that is, a probability of 33%).

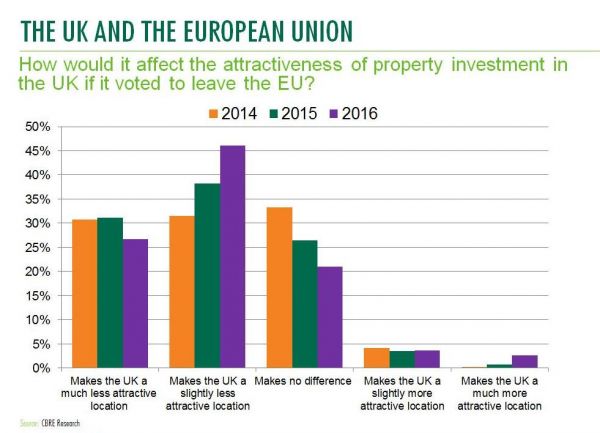

Most CBRE clients feel that leaving the EU would be negative for the UK’s real estate market. In a survey of clients active in the European investment market carried out last week, 73% said that Brexit would make the UK a less attractive place to invest against just 7% who thought it would increase the UK’s attractiveness. When we compare this result with the same question put to clients at the start of 2014 and 2015, attitudes appear to have hardened. Those in the ‘makes no difference’ camp appear to have decided, as the prospect moves closer, that ‘Brexit’ would make the UK a less attractive prospect.

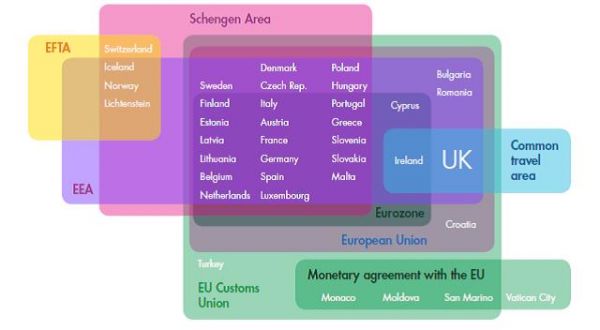

One of the difficulties in coming to a judgement is that we have very little idea what would replace the UK’s membership of the EU. There is a myriad of different treaty arrangements that cover relationships between groups of European countries, including the EEA (European Economic Area), EFTA (European Free trade Area) and the EU Customs area. Each type of relationship carries with it different sets of rights and obligations.

The EU treaty (Lisbon Treaty – 2007) allows two years for negotiations on the terms of exit once a country has served notice and nearly all of this would probably be needed to come to a final arrangement.

The sheer length of the period of uncertainty that would follow a ‘leave’ vote is a problem in itself. Leading up to the 2014 referendum on independence for Scotland there was a period for a few months before the vote when investors delayed decision making. In some instances deals were done, but with completion delayed and get-out clauses for buyers if the vote went for independence. After the vote the market returned to normal very quickly. Similar effects could be seen in the run up to the UK’s EU referendum (which is now only three months away). However, an exit vote would extend the period of uncertainty, potentially for a further two years.

On the other hand, if the UK votes to remain in the EU as expected, we think that there would be a ‘catch up’ effect in property market decisions in the second half of 2016 and when we look back at 2016 as a whole, investment activity might simply look more volatile, rather than lower than normal.

This article was written by Michael Haddock, Senior Director, EMEA Research, CBRE, for the CBRE Capital Watch blog.