JLL experts present two researched on the Q1 2017 Moscow & St. Petersburg hotel market results

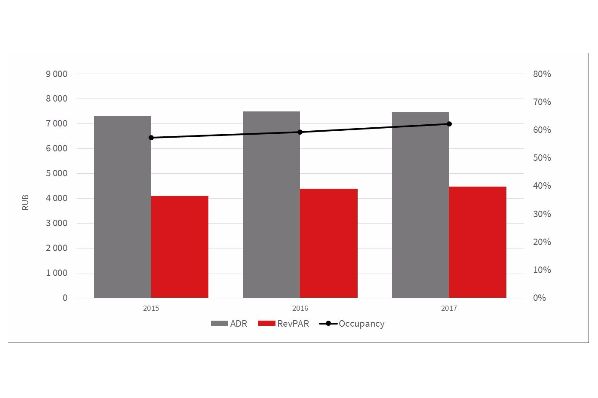

Moscow

Tatiana Veller, Head of JLL Hotels & Hospitality Group, Russia & CIS, says: “The market in the Russian capital is still riding strong, gaining volume of rooms sold in most segments and rates in some. Overall, the weighted market average occupancy of the quality hotels in the Russian capital had risen 2.6 ppt, and reached 62.1%, the highest Q1 YTD number in at least 5 years. Average marketwide ADR has dropped by mere RUB 44, representing a 0.6% loss, to 7,450 RUB . RevPAR still managed to climb a healthy 2,2% - to 4,480 RUB .”

Surprisingly, the segment in this quarter that lost a little bit on all fronts first time in at least 4 years was Luxury. Occupancy here dropped by 3 ppt (to 55%), rate by 1% (to 17,250 RUB ), and as a result the revenue per available room was 6% less, 9,450 RUB . “This is probably because the segment has been riding high and making large gains in many previous periods or maybe because the ruble had been appreciating further against hard currencies, and splurging on unreasonably high-end accommodation became less affordable for foreign traveler.” – Tatiana Veller comments.

The suburban resorts in the Moscow Region also had a good start to the year. Here RevPAR grew by 6% – to 2,500 RUB – due to an increase in the average rate by 11%, to almost 5,500 RUB. At the same time, the occupancy dropped by 2 ppt, to 46% amidst growing prices.

St. Petersburg

The occupancy of hotels in both Luxury and Midscale segments fell to 38% in Q1; the first case, the drop was 3.4 ppt in comparison with the same period of previous year, in the second – only by 0.5 ppt. The most expensive segment of St. Petersburg hotel market strengthened its price position, gaining 7% in ADR (to 11,500 RUB ), and was thus able to slow down the RevPAR decrease – it fell by only 1.5%. The Midscale segment, due to a very marginal loss in occupancy and growth in rates for a second consecutive year (an increase of 3.5%, up to 2,200 RUB), also managed to raise rooms revenues by 2%.

Tatiana Veller comments: “First months of the year are traditionally quiet for St. Petersburg’s hotel market, and this year was no exception. For the fourth consecutive year, the occupancy of quality hotels in this period fluctuated between 38-39%; past quarter it was almost equal to previous year's level – 38.7%. hotels continued to increase the weighted market average rate– by 6% compared to the same period in 2016, up to 3,600 RUB. As a result, the revenue per available room (RevPAR) grew by 4%, to 1,600 RUB.”

“The reason for this dynamic in the most expensive and most affordable segments of quality market most likely lies in the nature of demand: both luxury and midscale segments are fueled by tourists. But while in the luxury it is mostly frequent individual travelers (FIT) with high disposable incomes, in the midscale it is Russian or Asian touristic groups; both are subject to fluctuations due to the ruble exchange rate dynamics and weather conditions.” – Tatiana Veller comments. – “The remaining segments are primarily filled by business demand, thus are less volatile and have a different seasonality; as a result, these hotels continue to show growth in the three main operating indices – occupancy, ADR and RevPAR.”