SUMMARY

The economic situation in the Euro area continues to disappoint. GDP was down 0.2% q-o-q in Q1 2013, for the sixth consecutive quarter. Moreover, confidence indicators remain extremely low by historic standards and signal that activity might fall again in Q2 although at a slower pace. For the whole year, GDP might decrease by around 0.8%. Even though it is not immune to the global slowdown, Germany continues to outperform its peers. Thanks to strong domestic demand, Germany will be the only Euro area economy to record a positive growth rate. Conversely, France’s domestic demand will be dragged down by tighter fiscal policy. Activity in Spain and Italy remains subdued constrained by tight credit and tough labor market conditions. In the UK, growth returned in Q1 (+0.3%) but is expected to remain feeble over 2013.

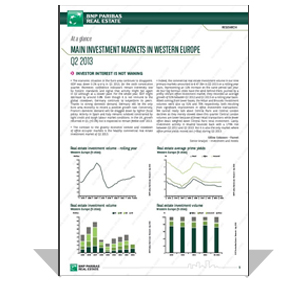

The contrast to the gloomy economic context and slowdown of office occupier markets is the healthy commercial real estate investment market of Q2 2013.

The commercial real estate investment volume in the nine primary markets investigated amounted to € 47.3 bn in Q2 2013 on a rolling year basis, representing an 11% increase on the same period last year. All four big German cities have the wind behind them, pushed by a pretty vibrant office investment market; they recorded an average growth of 52% between Q2 2012 and Q2 2013 on a rolling year basis. Albeit coming from lower bases, the Milan and Brussels investment volumes were also up 51% and 70% respectively, both resulting from significant improvement in office investment transactions. We cannot really talk about Central Paris and Central London declines as they merely slowed down this quarter. Central London volumes are lower because of fewer retail transactions while fewer office deals weighed down Central Paris total investment. Lastly, investment activity in Madrid bounced back with a 179% rise between Q2 2012 and Q2 2013. But it is also the only market where office prime yields moved out (+5bp) during Q2 2013.

(This article features excerpts from the full report – please download it here)