Investors in European listed property companies will benefit from about two years of low interest rates, rental growth and rising asset values, J.P. Morgan Chase & Co. analyst Tim Leckie told the European Public Real Estate Association’s (EPRA) annual conference on Wednesday.

Tim Leckie, J.P. Morgan’s real estate analyst, said: “Rental growth is spreading to Germany, Spain and Ireland after appearing first in the U.K. and this is very positive for net asset values of listed property companies. The summer’s turmoil in financial markets has probably pushed back the lift-off point for interest rates or flattens the speed at which they will rise. This means for the next 24 months or so we will have a continuation of the positive environment for the property industry: broadening rental growth and rising property values against a backdrop of historically low interest rates.”

The slide last month of global stock markets presents an attractive opportunity to buy listed real estate stocks to capture the rental growth and the appreciation in property values, according to the latest research by Leckie and fellow J.P. Morgan analyst Neil Green.

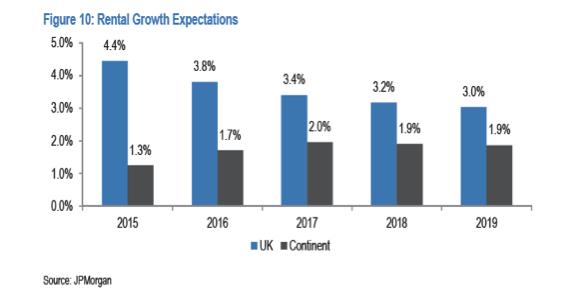

The U.K. currently offers the best prospects in Europe, with the IPD All Property Index showing that rents have risen by 1.2% since March. The pace of rental increases will slow steadily through 2019, Leckie forecasts.

Europe’s fastest rental growth is in London, with the cost of occupying offices in the City of London financial district or the West End rising by 44% and 34% respectively since the first quarter of 2009. By contrast, the office markets of Europe’s other major cities have fallen or grown by no more than 5% in the same period, Leckie said. A pipeline of new developments in the City office market means that rents will probably turn negative from 2018 due to oversupply, Leckie warned.

In continental Europe, rental growth is concentrated mainly in the German, Spanish and Irish markets, according to the J.P. Morgan analysis.

Supply constraints and falling vacancy rates will lift office rents in Frankfurt, German residential assets are increasing rents by 2-3% a year and shopping centre rents in Europe’s largest economy will strengthen as low unemployment, consumer confidence and low inflation drive retail sales higher.

The recovery in the Irish economy, falling vacancies and supply constraints mean that the Dublin office market can expect annual rental growth of 12%, while similar characteristics will start to feed through into 10% annual growth in rents in Madrid from next year, J.P. Morgan predicts.

In Amsterdam office rents may be approaching their low point, while in Paris there is no evidence of a pick-up in rental growth to warrant the considerable appreciation of office values, suggesting that assets may be overvalued, the research shows.

Indications of measured interest rate increases by the Bank of England for the next three years and prospects of the European Central Bank holding off until late 2017 or early 2018 before raising rates means that there is ample scope for property values to continue to rise when capital growth is supported by rising rents, J.P. Morgan said. Listed property company assets in continental Europe yield on average 3.2 percentage points more than 10-year benchmark bonds, which compares with the average 1.5 percentage point premium over the long term, the J.P. Morgan analyst noted.

Leckie concluded: “The benign interest rate outlook means that with property yields still at a significant premium to benchmark interest rates, there is still scope for capital appreciation for real estate assets across Europe. This is particularly the case when there is rental growth to support these higher values. These conditions underpin why we see good value in Europe’s listed property sector, offering a potential 16% upside to investors.”

Source: J.P. Morgan Chase & Co