Trying to navigate the European real estate markets as confidence and output wanes has proven to be challenging. Without economic growth, it is unsurprising that there has been little noticeable shift in real estate investor preferences. As predicted, leasing and investment activity has weakened and varies greatly depending on quality and location. Competition for prime assets has remained fierce, anchored by an investor search for real yield and added risk aversion.

Confidence beyond this narrow market spectrum has been restricted to opportunistic players, although this also reflects a lack of available finance as banks have continued to tactically reduce their real estate exposure. Talk of a Eurozone break-up has rightly receded, but the region is poised to remain in recession. Financial markets have responded well to Mario Draghi’s promise to support the euro, but in the real economy business confidence has contracted further.

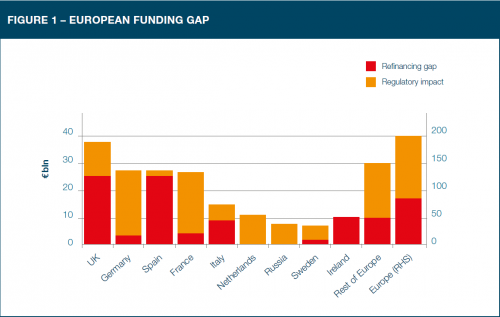

The debate now is whether government intervention has led to market bubbles rather than an expansion in real aggregate demand, as the economies of southern Europe will stay mired in recession in 2013 and economic indicators even point to a deterioration of output projections in the stronger economies of Germany, France and the Nordics. Funding tensions persist, most notably in Spain, where strains in the banking sector and capital outflows continue to limit finance to the private sector.

Elsewhere, low consumer confidence, unaided by rising unemployment, will ensure household spending is limited. A weakening in the euro exchange rate, once the uncertainty attached to the US fiscal stance has been removed, could aid exports but the wider implications of public and private sector deleveraging and attempts to reform across peripheral countries has weakened growth expectations. Talk of a European ‘lost decade’ is well-founded as the process of moving towards a fiscal and banking union will be slow and the recovery erratic.

Pricing levels expected to remain low in 2013

Few macroeconomic indicators are in expansionary territory, and as such, a rebound in occupier demand and a subsequent revival in rental levels seem unlikely until 2014 at the earliest. In peripheral European economies, further falls in rental tones are inevitable across both prime and secondary locations. In Germany, Austria, France, Finland and Sweden, relatively stronger economic fundamentals may be sufficient to avoid a major downturn in occupier demand, although heightened incentives are likely.

On a more positive note, a lack of development, which in itself is a factor of limited finance, should mitigate the downside risks for rents of good quality stock in 2013. Some may argue that pricing looks historically keen given the precarious nature of real estate fundamentals, but starved of yield, investors have little choice than to take the available income returns. Under our base assumption that the euro will survive, the implied risk premium over government bonds and elevated risk aversion should cushion fears of prime market pricing corrections.

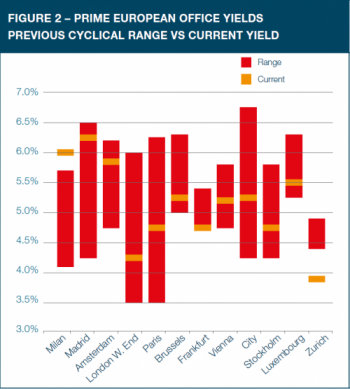

The ability of European REITs to raise capital at very attractive rates in 2012 has undoubtedly aided core valuations. The same, however, cannot be said for the direct market except for quality product. Downward adjustments for secondary product could stem from a combination of weaker occupier demand, further bank deleveraging and a hangover from 2012 repricing. Pricing will continue to be tested in Southern Europe and in the Netherlands across the board, whereas yields in France, Sweden and Austria will largely prove resilient, although a further hardening in Germany and Switzerland valuations is still a possibility.

Against such market angst and downgraded economic prospects, the resilient nature of quality real estate has been encouraging. Sufficient equity for prime persists, particularly from institutional investors and sovereign wealth groups who remain in a buying mode. Fears of a flurry of distressed sales have, however, been eroded by accommodative monetary policy.

Cross-border investment is likely to remain virtually non-existent in the periphery, but attractively priced opportunities will prove elusive as domestic competition for prime longincome assets persists, and expensive financing rates will penalize early risk-taking by international players. Resilient economic growth in core Europe should facilitate investor interest in good secondary real estate in that region, while prime yields are approaching new levels.

Retail warehousing and logistics: the rough diamonds of real estate

We believe there are a couple of areas that have been overlooked by investors since the downturn–perhaps due to perceived risk–that we think offer strong covenants and longterm growth prospects. These rough diamonds are retail warehousing and logistics. The retail warehouse sector in Europe suffered a sharp outward yield correction early in the downturn and has not recovered significantly since, offering good value for investors. We have always favored retail warehousing for the affordability it offers retailers compared to other retail formats, and the associated growth potential. This remains true and rents are now significantly cheaper following their recession declines. Investors still have the opportunity to capture the full rental recovery cycle in some markets.

While the pool of retail warehouse occupiers is relatively shallow in some markets, this is expected to improve as more retailers embrace the concept. Nevertheless, the current covenant quality on retail parks is generally very good. There are certainly risks to the retail occupier market, not least the continued diversion of sales to the internet but the retail warehouse sector is arguably better placed to fight against it and even exploit it. We expect to see rising demand from occupiers that seek clean, modern floor plates in accessible locations that can support multi-channel retailing and can accommodate the click & collect services that are currently enjoying very strong growth.

E-commerce is one of the fastest growing industries in Europe and while the roles of the traditional store and internet are becoming blurred, so are the roles of retail and logistics. This rapid growth in multichannel retailing is putting pressure on distribution channels and creating demand for property for storage of goods awaiting dispatch or collection. Hence we recognize the opportunity for real estate gains in the logistics sector, another asset type that has remained out of favor with mainstream investors.

Logistics is often portrayed as a niche property sector, which hugely understates its significance in advanced economies. More than half of the take-up of logistics space is ultimately for retail distribution, offering strong covenants in a growth sector. Retail is no longer just about distribution to shops but to homes too, with online shopping in Europe enjoying double-digit rates of growth over the last 10 years. Parts of Europe with large and affluent populations will attract increasing demand for logistics functions. Logistics operators will favor locations that are central to continental Europe, where population is dense and infrastructure is good. For investors, the sizeable yield differential compared to the office and retail sector and the long-term growth in demand at strategic locations make this sector a sound choice.

No significant changes expected in 2013

In summary, it is hard to envisage 2013 being significantly different from 2012, with performance relying on income security and active asset management. By the end of 2013, the economic future of Europe could start to take shape and investors will have to be ready to adapt quickly to a changing environment. As the outcome is strongly dependent on political factors, this could be a sell-off of exposures in the periphery with hopes for a strong recovery waning, as well as investors making their first commitment back into the shunned region on the back of encouraging economic numbers. Europe will prove a stock pickers’ market and investors need to be risk aware, not necessarily risk averse, in their investment procedure to achieve outperformance.

By Alice Breheny, Head of Research, Property, Henderson Global Investors

About Henderson Global Investors

Henderson Global Investors is a leading multi-asset independent investment management company managing €78.6 billion in assets. We are a major investor in the global property market with over 30 years in-depth experience working on behalf of segregated direct mandates, pooled funds, property securities and fund of funds clients. We have a global property presence with offices in London, Paris, Frankfurt, Luxembourg, Milan, Madrid, Stockholm, Vienna, Hamburg, Chicago, Hartford, Beijing, Hong Kong, Sydney and Singapore, managing €15.1 billion of property assets.

Henderson Global Investors

201 Bishopsgate

London EC2M 4AE

T: +44 (0)207 818 1818

W: www.henderson.com/property

Twitter: @HGiProperty