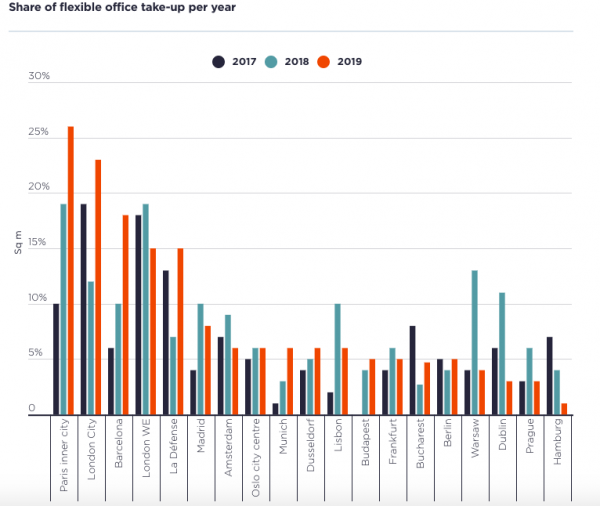

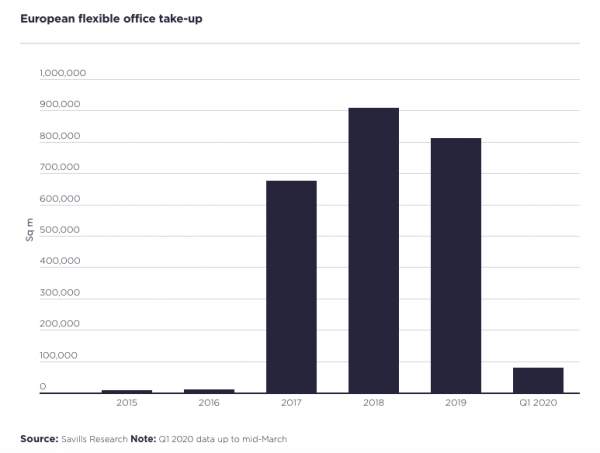

Over the past five years, about 2.5m m² of office space has been leased to flexible office providers across the 12 European markets that we monitor, accodring to the latest findings by Savills. The sector boomed between the years 2017–2019 with an average annual take-up of about 800,000m² or over 8% of the annual total on average across the 12 markets we monitor. WeWork has been driving at least one third of the activity between 2017–2019 across most markets. In 2019, the share of flexible office take-up was at 9.5%. The city with the highest share was Paris (inner city) at 25.6%, followed by London City at 23%, Barcelona at 18.1% and London West End at 15%. In all the remaining cities the share was below 10%.

In Q1 2020 (data up to mid-March), demand by flexible office providers has slowed down significantly, with the share of flexible office take-up at about 5% of the total on average. Overall total Q1 office take-up also dropped by 19% YoY on average, reflecting the persistent shortage of quality available space, as well as early concerns about the spread of coronavirus, which had already emerged in Asia. Savills believes that Q1 results do not yet fully reflect the impact of the lockdown due to the pandemic, but they mostly demonstrate that the flexible office sector has reached a level of maturity, with the larger players slowing down their expansion.

WeWork has suspended new openings and has shifted its focus on cutting costs and renegotiating leasing agreements with landlords. This is partly the result of the negative impact of the pandemic on demand for flexible office space, but predominantly because the company was already exposed to leasing obligations, which were much higher than their revenue. On the other hand, the second largest operator in this field IWG (through its brands Regus, Spaces etc.), which has accounted for about 20% of total leasing activity since 2015, was also less active at the beginning of this year, accounting for 9% of the total. Smaller players instead have been more acquisitive, and the average size of deal dropped by 18% from 3,150m² in 2019 to 2,600m² in Q1 2020. The quarterly data are usually quite volatile, but first indications (data up to mid-March) show that the market with the highest flexible office take-up was Paris Inner City (26, 755m²), followed by Berlin (9,635m²). Last year the largest market was the City of London (142,328m²), followed by Paris inner City (133,296m²) and Barcelona (68,960m²).

The flexible office market is amongst the sectors that are mostly exposed to the negative impact of the Covid-19 pandemic, after hospitality and retail. On the one hand, the lockdown measures that have forced millions of people to work from home and on the other hand the short-term nature of contracts, have left flexible offices with very low occupancy across Europe. Although many operators remain open, building occupancy is below 20%, with private offices remaining partly in use, while demand for co-working space is non-existent and communal areas are being closed. According to the latest global sentiment survey from Workthere, flexible office providers expect contract occupancy to be 71% at the end of May, which compares to 83% pre-Covid-19. Workthere has found that 33% of members of flexible offices have asked for some form of rent relief.

According to Workthere, 62% of flexible office providers globally are optimistic about the prospects for the sector over the next 12 months. In times of uncertainty, flexibility will be a sought after solution, as businesses might avoid long-term leasing commitments. Moreover, with more people working from home regularly, companies may choose to spread their office requirements across traditional and flexible office solutions in different locations. This may also lead to more demand for flexible office space in non-CBD locations and closer to transport hubs.At the same time, overall supply of office space is expected to remain tight, which should keep prime rental levels for traditional leases high. In Q1 the average office vacancy rate in the markets covered in this report was around 5%, and the office space in the pipeline for 2020 corresponds to 50% of last year’s take-up, across the markets analysed.

For the remaining of the year Savills does not expect flexible office providers to be acquisitive, as instead, their focus will be on maintaining their existing customer relations and on working together with their landlords, until the ‘next normal’ arrives. Besides, COVID-19 will accelerate the use of management agreements between landlords and operators, and we expect to see significantly fewer leases signed, as they seek a more partnership model going forward.